As of today, I've compiled the preliminary 2027 rate filings for the ACA-compliant individual and small group markets across 25 states (including the District of Columbia). So far, the weighted average increases being requested range from as little as 6.5% in Vermont to as much as 22.9% in Alaska. Interestingly, both of these states already have some of the highest individual market premiums for unsubsidized enrollees in the nation...over $1,000 per month per enrollee.

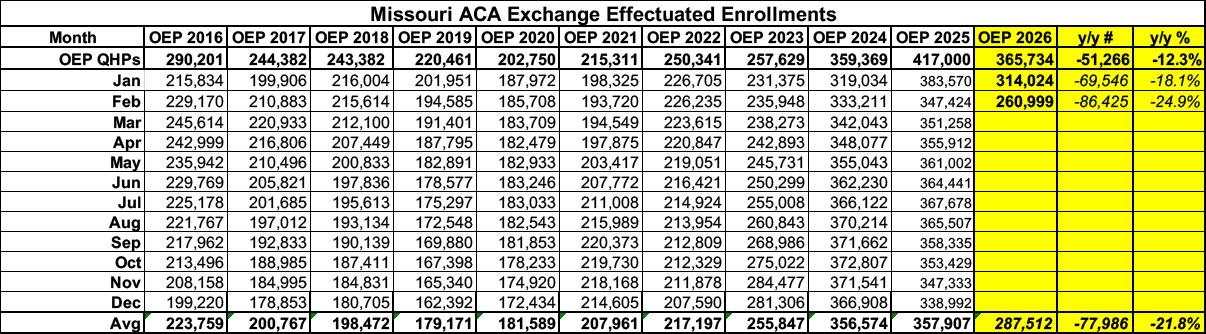

ACA exchange enrollment has dropped by a whopping 25% in Missouri since Congressional Republicans allowed the enhanced federal subsidies to expire at the end of last year.

Initial signups during Open Enrollment were already down over 12% vs. OEP 2025...but effectuated enrollment in was 18% year over year as of January and 25% lower in February. That's over 86,000 Missourians who have lost their individual market healthcare coverage.

Here's what this looks like visually, with both 2025 and 2019 (the last pre-COVID year, which didn't include the enhanced subsidies) included for comparison:

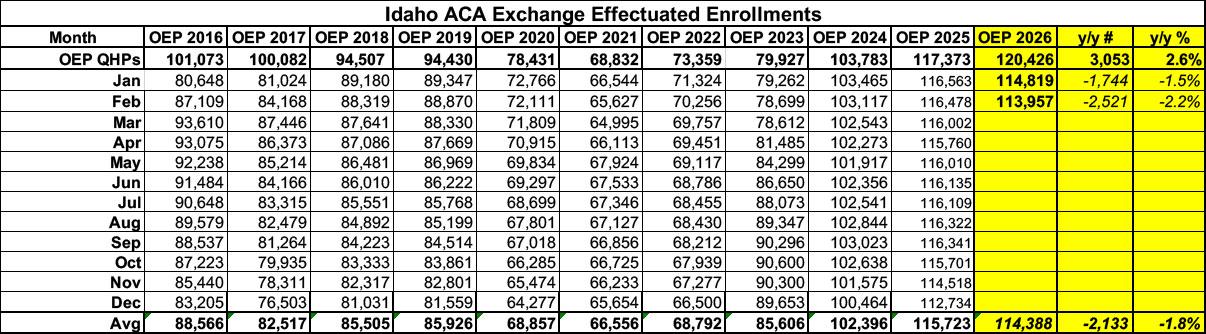

Idaho is one of a handful of states where plan selections during the 2026 Open Enrollment Period actually increased year over year, by around 2.6%, in spite of the enhanced federal subsidies expiring back in December.

Two months into the year, however, effectuated enrollment is actually down slightly (by around 2.2%, or roughly 2,500 enrollees).

Here's what this looks like visually, with both 2025 and 2019 (the last pre-COVID year, which didn't include the enhanced subsidies) included for comparison:

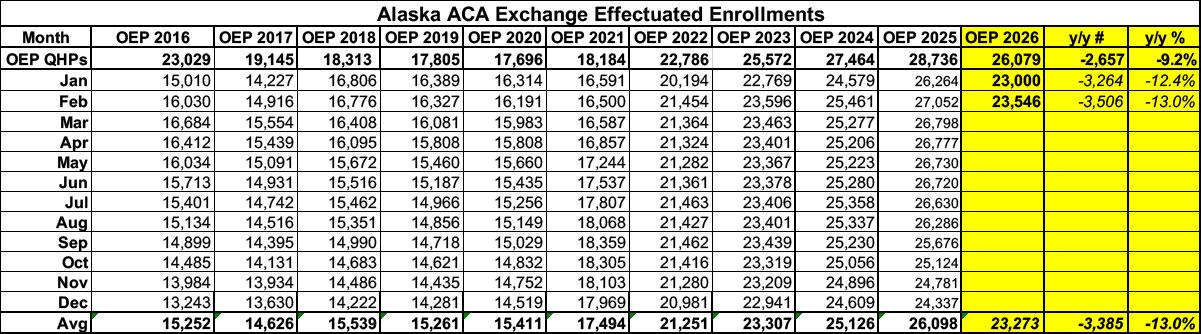

ACA exchange enrollment has dropped significantly in Alaska since Congressional Republicans allowed the enhanced federal subsidies to expire at the end of last year.

Initial signups during Open Enrollment were already down 9.2% vs. OEP 2025...but effectuated enrollment as of January 2026 was down over 12% year over year...increasing to a 13% drop as of February.

The good news, such as it is, is that due to Alaska having such a small ACA population to begin with, this only amounts to around 3,400 people losing coverage...which is small comfort if you're one of those 3,400 people, of course:

Here's what this looks like visually, with both 2025 and 2019 (the last pre-COVID year, which didn't include the enhanced subsidies) included for comparison:

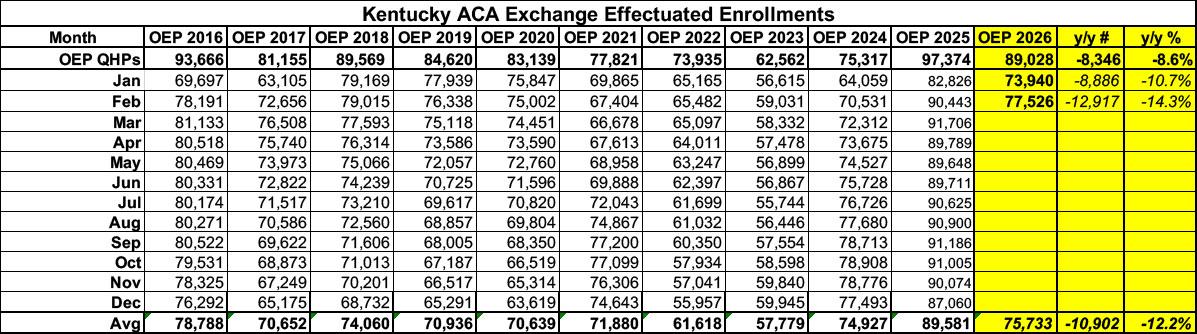

Before I begin, it's important to note that ACA exchange enrollment has dropped significantly in Kentucky since Congressional Republicans allowed the enhanced federal subsidies to expire at the end of last year.

Initial signups during Open Enrollment were down 8.6% vs. OEP 2025...but effectuated enrollment was down nealry 11% in January and over 14% as of February; on average nearly 11,000 Kentuckians lost ACA healthcare coverage in the first two months of 2026:

Here's what this looks like visually, with both 2025 and 2019 (the last pre-COVID year, which didn't include the enhanced subsidies) included for comparison:

Before I begin, it's important to note that ACA exchange enrollment has dropped in Hawaii since Congressional Republicans allowed the enhanced federal subsidies to expire at the end of last year. Fortunately, the raw number of enrollees who have lost coverage is pretty small due to:

a) Hawaii only having around 1.4 million residents to begin with and

b) Hawaii having a much more robust Employer-Sponsored Health Insurance mandate law than the ACA. Under the Hawaii Prepaid Health Care Act of 1974, employers are required to offer coverage to employees working at least 20 hours per week. In contrast, the federal Patient Protection and Affordable Care Act requires employers to offer coverage to employees working at least 30 hours per week.

As a result, Hawaii's individual/nongroup health insurance market is smaller as a percentage of the total population than it is in most other states.

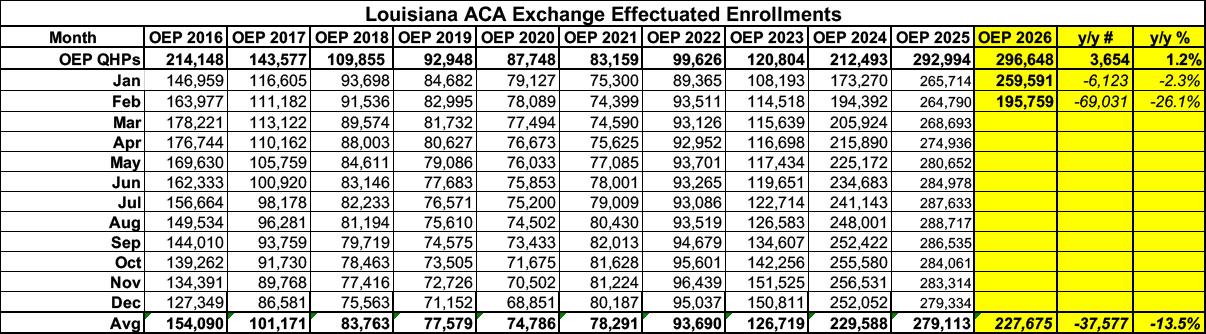

Before I begin, it's important to note that ACA exchange enrollment has plummeted in Louisiana since Congressional Republicans allowed the enhanced federal subsidies to expire at the end of last year.

Initial signups during the 2026 Open Enrollment Period were actually up slightly vs. OEP 2025...but actual effectuated enrollment was 2.3% lower as of January...and then fell off a cliff in February, with enrollment dropping a stunning 26% vs. a year earlier. That's over 69,000 Louisianans who were priced out of coverage in just the first two months of the year:

Here's what this looks like visually, with both 2025 and 2019 (the last pre-COVID year, which didn't include the enhanced subsidies) included for comparison:

Initial signups during Open Enrollment were only down about 2% vs. 2025..but effectuated enrollment began to drop immediately and has continued to drop every month since then.

As of June 2026, effectuated enrollment is down 8.4% vs. a year earlier, and is down 7.7% on average for the year so far. That's around 22,000 fewer Coloradans with ACA exchange coverage so far this year:

Recent federal changes are making it more difficult for Washingtonians to access and maintain health insurance. While hundreds of thousands rely on Washington Healthplanfinder to find and enroll in coverage, new federal policies will leave many residents at risk of losing the care they need.

We at Washington Health Benefit Exchange are still doing all we can to help residents get health and dental insurance, regardless of immigration status. However, due to H.R. 1 and new rules impacting marketplace coverage, there are changes regarding immigrant eligibility and how much people pay for health insurance.

As of October 1, 2025, people with Deferred Action for Childhood Arrivals (DACA) status no longer qualify for federal tax credits.

Before I begin, it's important to note that ACA exchange enrollment has dropped in Pennsylvania since Congressional Republicans allowed the enhanced federal subsidies to expire at the end of last year...although thanks to the state implementing fairly robust Premium Alignment pricing, it's not nearly as dramatic a drop-off as in most other states.

Initial signups during Open Enrollment were actually slightly higher than last year...but effectuated enrollment began to drop starting in February and has continued to drop at an increasing rate every month since then. As of July 2026, effectuated enrollment is down more than 10% vs. a year earlier, and it's down nearly 4% on average for the year so far. That's 48,000 fewer Pennsylvanians with ACA exchange coverage as of July: